Model Specification Test In Econometrics

The asymptotic power of a statistical test depends on the model. In order to make the model as realistic as possible the analyst may include as many as possible explanatory variables.

2

75 Model Specification for Multiple Regression.

Model specification test in econometrics. 1 R2new n number of parameters in the new model 4. Test model specification using the link test. In such selections there can be two types of incorrect model specifications.

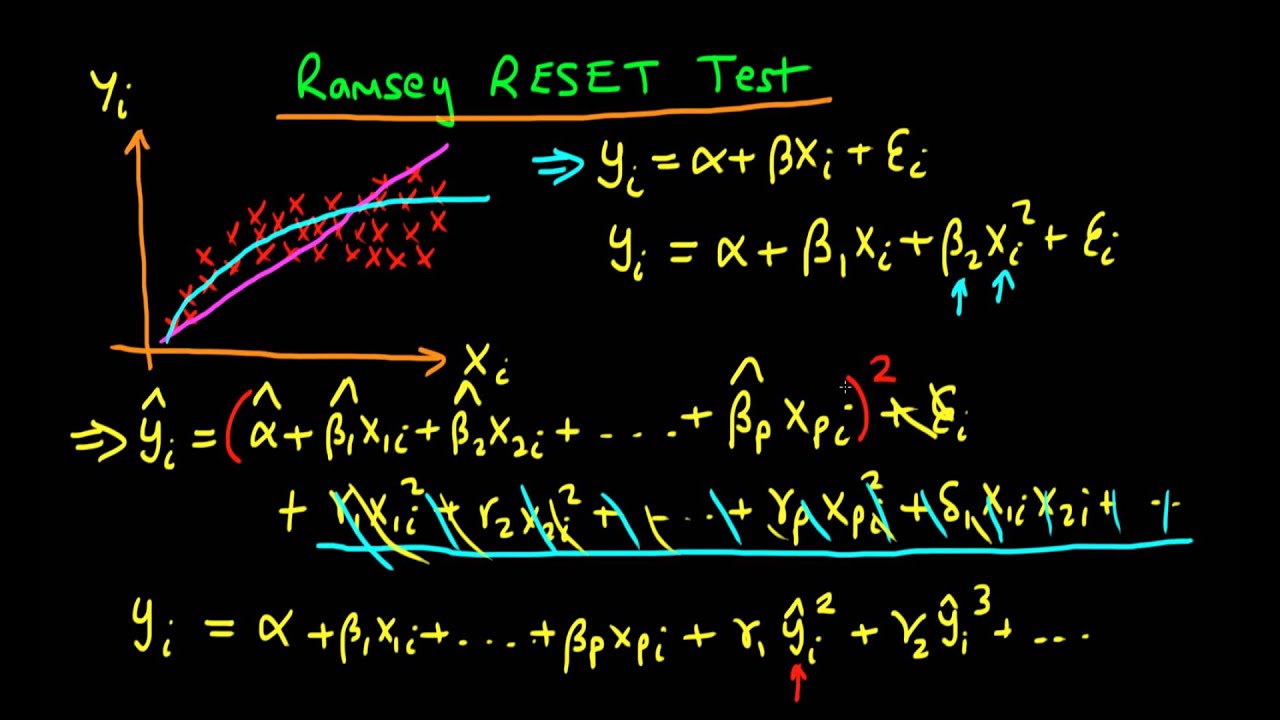

Test for missing variables using the Ramsey regression specification error test. Using the result that under the null hypothesis of no misspecification an asymptotically efficient estimator must have zero asymptotic covariance with its difference from a consistent but asymptotically inefficient estimator specification tests are devised for a number of model specifications in econometrics. The economic models are formulated in an empirically testable form.

In this lecture we discussed model specification. Local power is calculated for small departures from the null hypothesis. Using the result that under the null hypothesis of no misspecification an asymptotically efficient estimator must have zero asymptotic covariance with its difference from a consistent but asymptotically inefficient estimator specification tests are devised for a number of model specifications in econometrics.

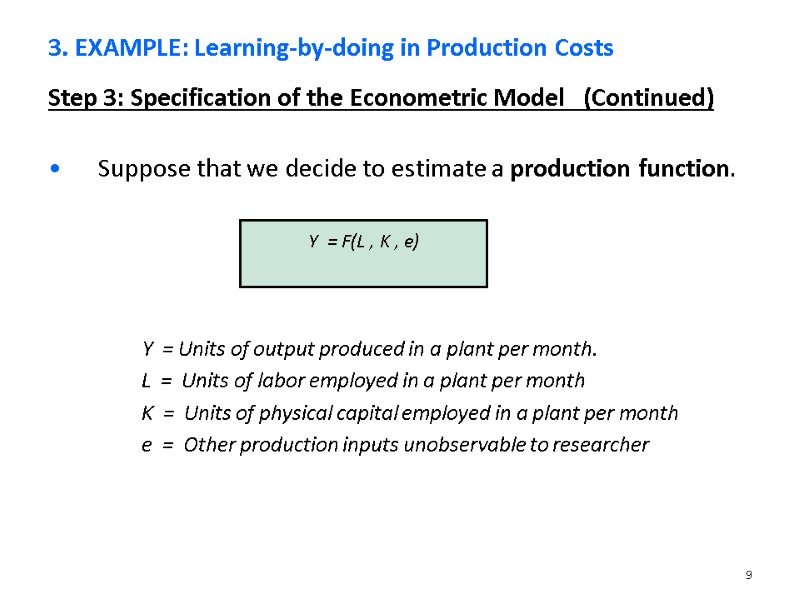

Slide 81 Undergraduate Econometrics 2nd Edition-Chapter 8 Chapter 8 The Multiple Regression Model. Omitting a Relevant Variable I In econometrics this issue is known as omitting a relevant variable if 2 6 0 and this is a type of misspeci cation The big question then is what is the e ect of omitting a relevant variable. Formulation and specification of econometric models.

Econometric methods offer. Specification tests in econometrics. We looked at the case we have an under-fitted model in which the researcher omits relevant variables.

In econometrics specification tests have been constructed to verify the validity of one specification at a time. Step 3 - If the restricted model is accepted test its residuals to ensure. In the example given above relating personal income to schooling and job experience if the assumptions of the model are correct then the least squares estimates of the parameters ρ displaystyle rho and β displaystyle beta will be efficient and unbiased.

An instrumental variable test as well as tests for a time series cross section model and the simultaneous equation model are presented. We can test which model to use model A or model B and we can test it with the help of the Davidson MacKinnon tests. It is argued that most of these tests are not in general robust in the presence of other misspecifications so their application may result in misleading conclusions.

Local power is calculated for. This tutorial builds on the first four econometrics tutorials. However there are some guidelines on how to proceed.

After completing this tutorial you should be able to. If the computed F value is significant say at the 5 percent level one can accept the hypothesis that the model is mis-specified. Econometricians are usually interested in testing non nested model specifications.

Number of model specifications in econometrics. Such models differ due to different choice of functional form specification of the stochastic structure of the variables etc. Correct specification is called pre-test bias.

Estimation and testing of models. The Ramsey RESET test can help test for specification error in regression analysis. Testing the Specification of Econometric Models in Regression and Non-Regression Directions.

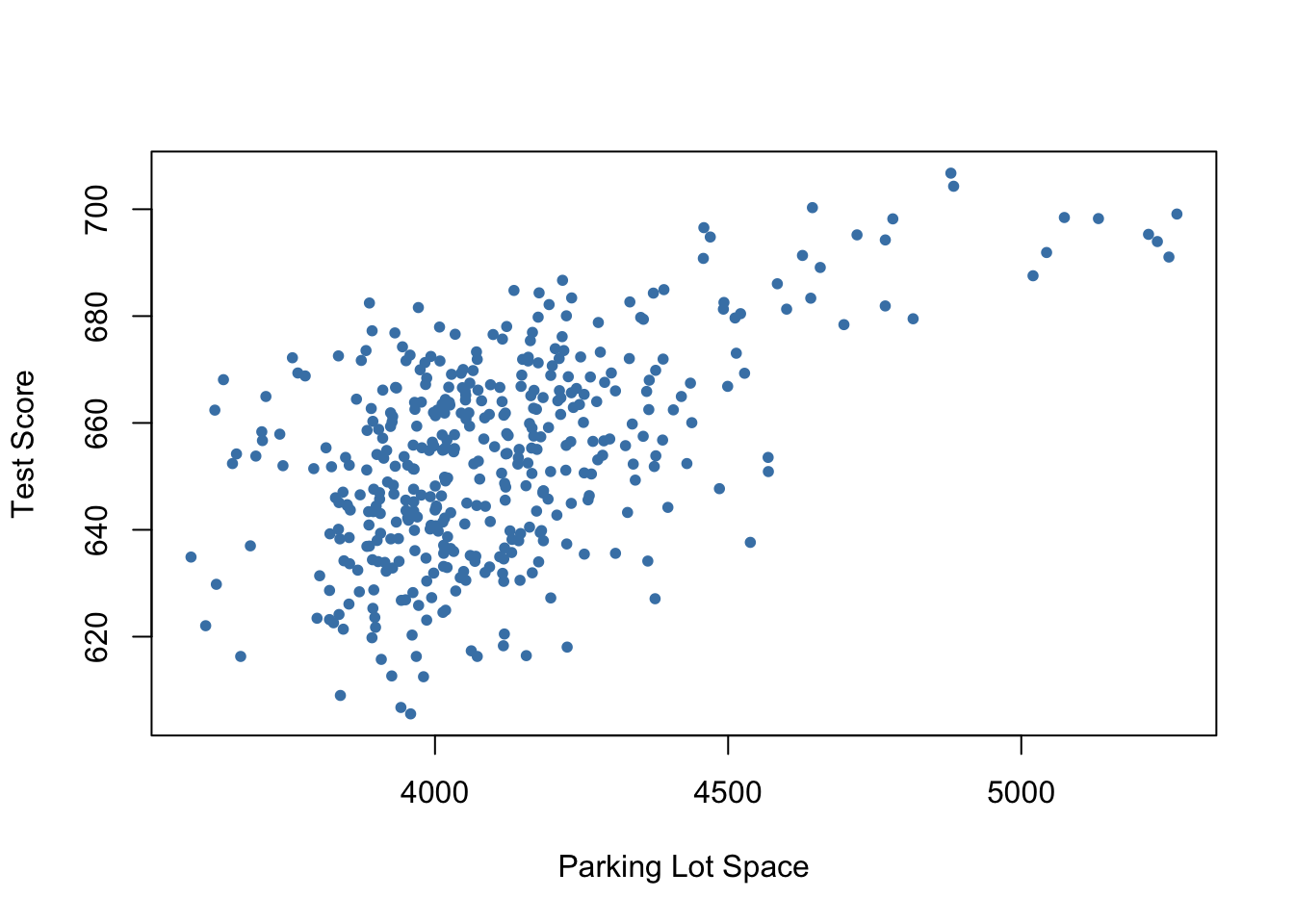

Choosing a regression specification ie selecting the variables to be included in a regression model is a difficult task. This tutorial demonstrates how to test for influential data after OLS regression. In order to make the model as simple as possible one may include only fewer number of explanatory variables.

It is argued that most of these tests are not in general robust in the presence of other misspecifications so their application may result in misleading conclusions. The goal is clear. An empirical model provides evidence that unobserved individual factors are present which.

Further if the functional form is properly specified RESET has no power for detecting heteroske- dasticity. Obtaining an unbiased and precise estimate of the causal effect of interest. Pre-testing also called sequential estimation data mining is common in practice.

F R2new R2oldnumber of new regressors. Several econometric models can be derived from an economic model. The answer is given in the equation below.

For example we have two alternative theories which bring us to two different regression models. In econometrics specification tests have been constructed to verify the validity of one specification at a time. - Lagrange Multiplier LM Test for Adding Variables.

Using the Lagrange Multiplier principle we develop efficient test procedures that are capable of testing a number of specifications. Our course starts with introductory lectures on simple and multiple regression followed by topics of special interest to deal with model specification endogenous variables binary choice data and time series data. It is suggested that you complete those tutorials prior to starting this one.

The bottom line is that RESET is a functional form test and nothing more. His research has focused on model specification issues in econometrics in particular consistent model specification testing of cross-section and time series models nonparametric estimation unit root cointegration and co-trending testing econometric analysis of dynamic stochastic general equilibrium models and more recently semi-nonparametric. Hypothesis Tests and the Use of Nonsample Information An important new development that we encounter in this chapter is using the F- distribution to simultaneously test a null hypothesis consisting of two or more.

Pendent variables in the model see Wooldridge 1995 for a precise statement. You learn these key topics in econometrics by watching the videos with in-video quizzes and by making post-video training exercises.

1 What Is Econometrics Steps In Empirical Economic

Regression Diagnostic Iv Model Specification Errors Ppt Download

7 5 Model Specification For Multiple Regression Introduction To Econometrics With R

Pdf Testing The Specification Of Econometric Models In Regression And Non Regression Directions

Regression Diagnostic Iv Model Specification Errors Ppt Download

Lecture 9 Model Specification Youtube

Econometrics Model Specification Youtube

Pdf Specification Tests In Econometrics Semantic Scholar

2

Pdf Model Specification Tests And Artificial Regression

Pdf Some Specification Tests For The Linear Regression Model

Lecture 9 Model Specification Youtube

Cruncheconometrix Beginners Econometrics This Is How To Specify Ardl Models Facebook

Hackl Advanced Econometrics Ppt Download

Ramsey Reset Test For Functional Misspecification Youtube

Lecture 1 Introduction To Econometrics Online Presentation

Pdf Specification Tests In Econometrics Semantic Scholar

Regression Diagnostic Iv Model Specification Errors Ppt Download

Econometrics Model Specification Youtube

Posting Komentar untuk "Model Specification Test In Econometrics"